Thus, the equations showthat the total costs of a producing department includes the department’s direct cost (Di), plus the allocations from the various service departments(i.e., the sum of [(Kji)(Sj)]). Although it is the most accurate, it is also the most complicated. In the reciprocal method, the relationship between the service departments is recognized. This means service department costs are allocated to and from the other service departments. The final method, is the reciprocal method.Although it is the most accurate, it is also the most complicated.In the reciprocal method, the relationship between the servicedepartments is recognized.

Allocating Fully Reciprocated Costs to Production Departments

- In the second step, the equations for the service departments are solved first in the sequence established by the rules mentioned above.

- However, a new public utility has recently offered to provide electric power to the plant for 4.5 cents per kilowatt hour.

- Examples of operating departments are the assembly departments of manufacturing firms and the departments in hotels that take and confirm reservations.

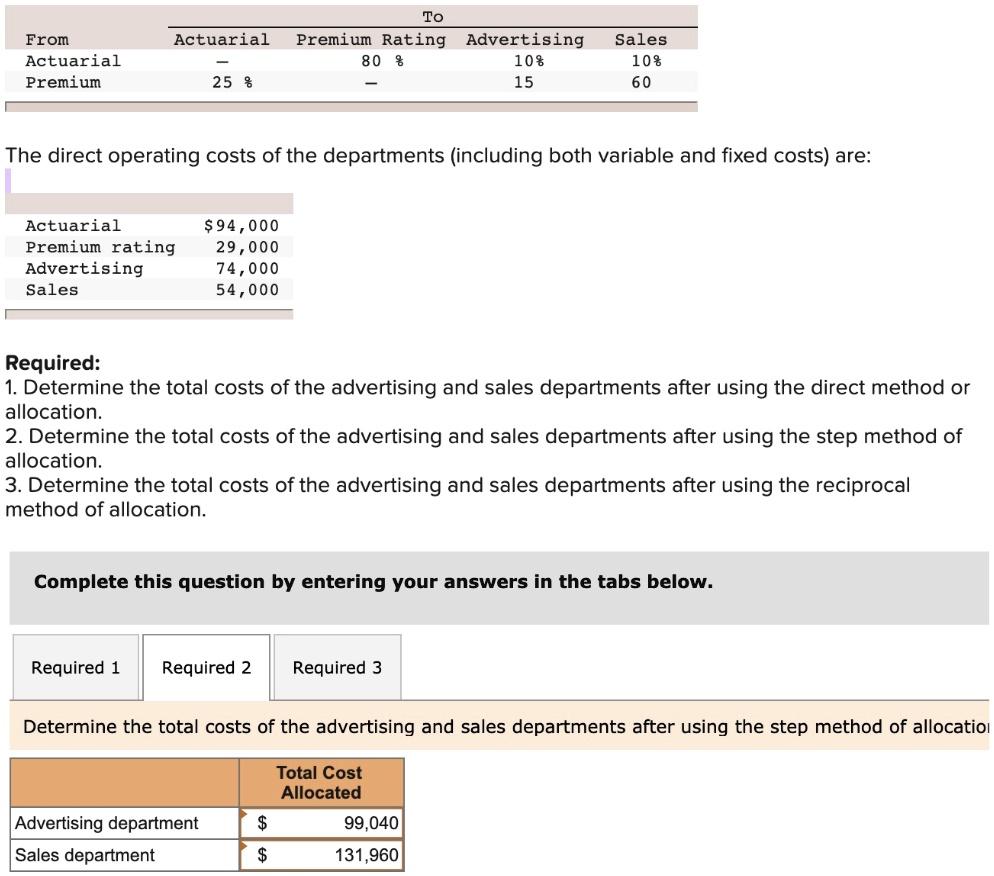

The products obtained from a hog such as the chops, ham, and bacon are jointproducts. In fact, joint products are common in a variety of industries including petroleum, flour milling, meat packing, dairy, coal, copper, salt,chemicals, soap, gas, leather, and tobacco. The term “by-products” refers to a sub-category of joint products that have relatively insignificantsales depreciation of assets values as a proportion of the value of the entire group from which they are derived. Since maintenance costs are allocated to administration and administration cost is allocated to maintenance — things get interesting. You will need to determine the TOTAL cost being allocated to both the Administration and Maintenance Departments first.

AccountingTools

The allocationscreate equal profit ratios for both products, which insures that the resulting inventory values for both products are below their market values.6This result will not create any special problems for accounting. From the management decision perspective, these results are not useful, but at least theydo not support an incorrect decision with regard to product D. To illustrate the advantages of the dual rate or flexible budget method, consider the revised information that appears in Exhibit 6-9. This exhibit shows the same data thatappears in Exhibit 6-3 except service costs are separated into fixed and variable elements. The total producing department costs, after all allocations, is equal to the total direct costs budgeted, i.e., $500,000 (Seethe note at the bottom of Exhibit 6-4).

Activity Sampling (Work Sampling): Unveiling Insights into Work Efficiency

For example, the power departmentprovides electric power to the maintenance department and the maintenance department provides repair and maintenance to the power department. Theserelationships affect the choice of allocation methods, as well as the accuracy of the first stage cost allocations. From the management decision perspective, joint cost allocations are useless because they are not relevant in decisions concerning the separate products. For example, decisionsconcerning whether to continue or discontinue producing the joint products depend on their combined value, not the value of any particular product at thesplit-off point. Therefore, it has been argued that the joint costs should not be allocated at all. However, if the joint costs are not allocated, a valuestill needs to be placed on the unsold inventory for financial reporting purposes.

A plant wide rate based on machine hours would provide accurate product costs.c. Activity based rates would be needed to provide accurate product costs since direct labor is not used in proportion to machine hours.d. Activity-Based Costing (ABC) represents a significant evolution in cost allocation methods, particularly suited for organizations with diverse and complex operations. Unlike traditional methods that may allocate costs based on simplistic metrics like direct labor hours or machine hours, ABC delves deeper into the specific activities that drive costs.

Calculating Fully Reciprocated Costs

The three alternative methods of allocating service department costs to users are summarized in Exhibit 6-13. From the service cost perspective, the differences are more significant. Both the direct and step-down methods understate power costs by $9,585, or approximately 9.6%. On the otherhand, maintenance costs are understated by $17,261 using the direct method and $6,150 using the step-down method. These differences are likely to besignificant in terms of evaluating the service department costs, particularly in cases where a “make or buy” (outsourcing) decision is involved. The Cutright Company has a small factory with two service departments and two producing departments.

The Assembly Department manager is likely to complain that neither of the allocations in Exhibit 6-11 is equitable. He or she might logically argue that the dual rate method illustratedabove assigns the Power Department’s idle capacity costs to the Assembly Department. These idle capacity costs will in turn be allocated to the AssemblyDepartment’s products. Using a single budgeted rate, rather than either a single actual rate or dual rate (Exhibit 6-11) will normalize the service costsallocations, provide more timely costing and aid in evaluating the service departments. Conceptually, this is the same logical argument discussed inChapter 4 under the heading of reasons for using a predetermined overhead rate.

These activities could range from procurement and production to marketing and customer service. Each activity is then assigned a cost driver, which is a factor that directly influences the cost of the activity. For example, the cost driver for the procurement activity might be the number of purchase orders processed, while the cost driver for production could be the number of machine setups required. By linking costs to these drivers, ABC provides a more granular view of how resources are consumed across different activities. Discover modern cost allocation methods to enhance management efficiency and optimize resource distribution in multi-department organizations. In this situation, service cost centre overheads are simply ‘shared out’ on the basis of usage.

Service departments aid multiple production departments at the same time, and accountants must allocate and account for all of these costs. It is crucial that these service department costs be allocated to the operating departments so that the costs of conducting business in the operating departments are clearly and accurately reflected. Departmental rates based on machine hours would provide accurate product costs.b.